If you are a self-employed individual in Singapore, there are several aspects of finances that you should pay close attention to. Managing your finances effectively is crucial for the success and sustainability of your self-employment/ hustling life~

Here are 6 important things to keep in mind:

- Know your taxes!

Understand your tax responsibilities and ensure timely filing of your tax returns. Familiarize yourself with the applicable tax rates and deductions available for self-employed individuals.

Tax Reliefs: https://www.iras.gov.sg/taxes/individual-income-tax/basics-of-individual-income-tax/tax-reliefs-rebates-and-deductions/tax-reliefs

Guides available on IRAS: https://www.iras.gov.sg/taxes/individual-income-tax/self-employed-and-partnerships/tax-obligations-by-industry-trade-or-profession - Keep it organised!

Maintain accurate financial records to track your income and expenses. As you income /expenses go up, consider using accounting software or hiring a professional to assist you with bookkeeping tasks. It also gives you a better idea of how profitable you really are. - Money moves! So take note of your budget & cash flow.

Create a realistic budget to allocate your income and expenses effectively. Ensure you have sufficient funds for both personal and business needs. Cash is queen. Cashflow is king! - Future Planning -Plan for your retirement.

Unlike employees, self-employed individuals do not have mandatory Central Provident Fund (CPF) contributions. Therefore, it is crucial to plan and save for your retirement through alternative means, such as voluntary CPF contributions or other retirement savings vehicles to ensure streams of guaranteed income in retirement.

Note: Self employed individuals are also required to make mandatory Medisave contribution. You can find out more here: https://www.cpf.gov.sg/member/growing-your-savings/cpf-contributions/saving-as-a-self-employed-person - Protect yourself from life’s surprises with insurance.

As self-employed, you do not enjoy employee insurance benefits. Take care of yourself, check out health insurance, critical illness insurance, and business insurance. Ensure that you have adequate coverage to protect yourself and your business from unexpected events.

At the different stages, different vehicles may work to your favor. In the early years, a term plan may be idea to keep premiums low. But if budget allows, a life plan may be a better solution in the long run. - Stay in the know, continue learning.

Stay updated with the latest financial regulations, tax changes, and government schemes that may benefit self-employed individuals. Attend workshops or seek professional advice to level up your financial knowledge and skills.

OR, you can also reach out to me, a Certified Financial Planner @ Financial Alliance to find out more.

By paying attention to these key financial aspects, you can better manage your finances as a self-employed 😉

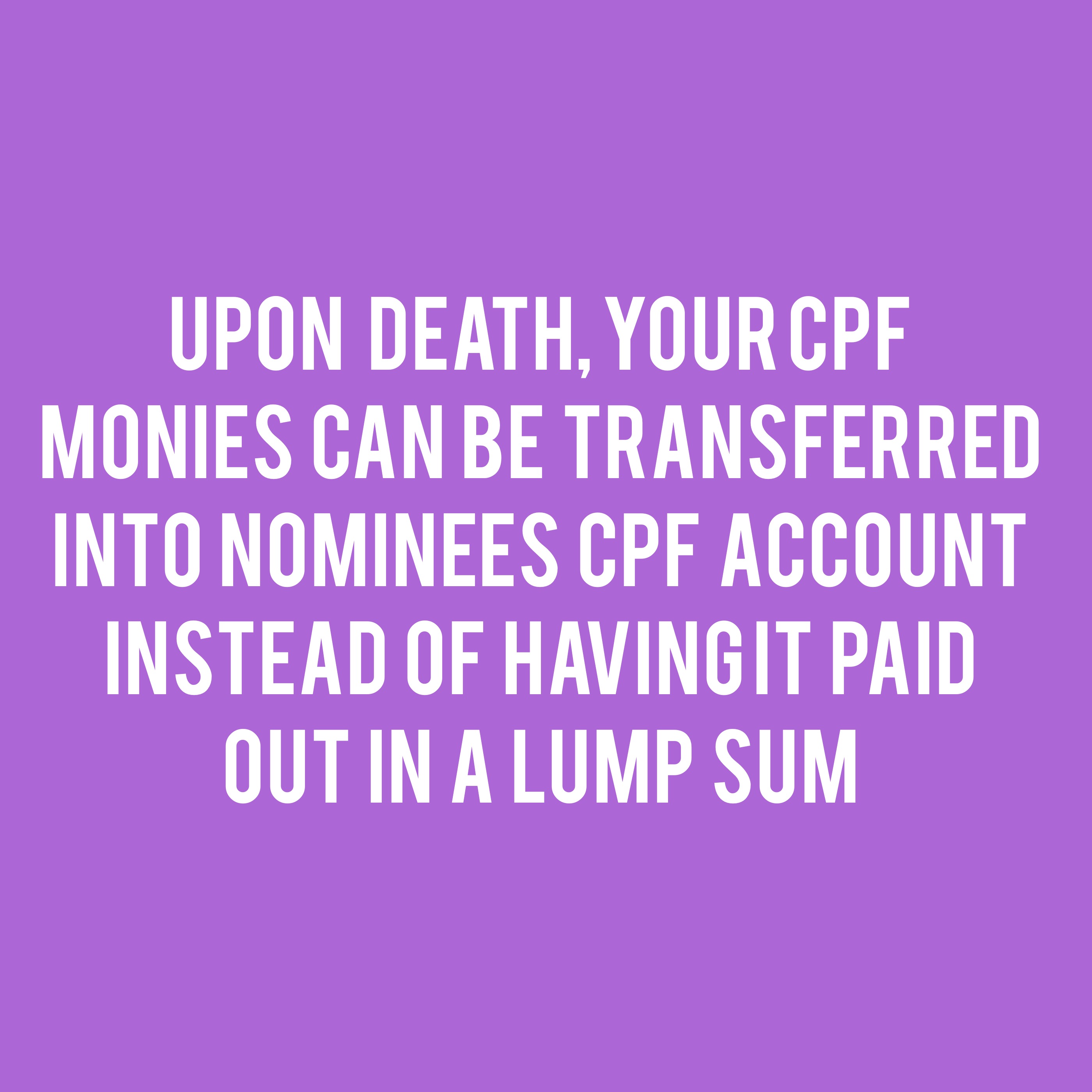

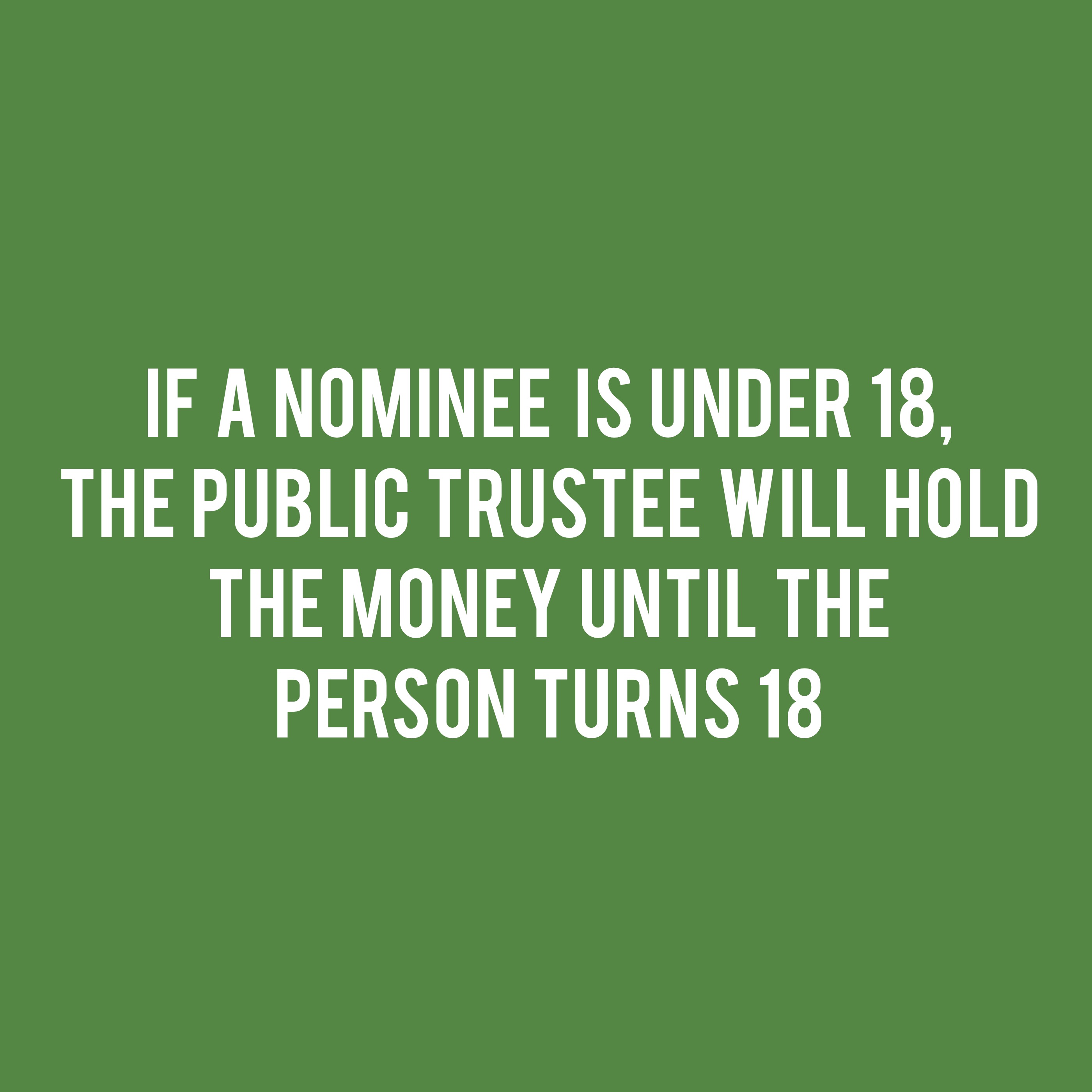

Unknown to many, CPF actually has the special needs saving scheme that can help parents of children with special needs to save for their long-term care needs. Parents can nominate their children to receive monthly disbursements from the parent’s CPF savings after death. This scheme is administered by the Special Needs Trust Co and is probably worth looking at if of relevance.

Unknown to many, CPF actually has the special needs saving scheme that can help parents of children with special needs to save for their long-term care needs. Parents can nominate their children to receive monthly disbursements from the parent’s CPF savings after death. This scheme is administered by the Special Needs Trust Co and is probably worth looking at if of relevance.