Singlife MyShield Plan Coverage (with or without the existing copayment riders): 5X MediShield Life Limit

Across all 7 insurers, Singlife has the lowest cover as there are no extra benefit/coverage from having a rider (HealthPlus etc).

However, Singlife is also the only insurer (as of the date of this post) who has launched a cancer medical reimbursement plan that will cover the charges for outpatient cancer drug treatments (including drugs not on the cancer drug list) at a much higher limit. It also covers selected cancer treatments such as Inpatient and Outpatient Cell, Tissue and Gene Therapy and Proton Beam Therapy.

Coverage is as charged and the plan will cover, in excess of deductible, up to S$1.5million per policy year.

Conclusion: If you are Singlife Policyholder and if health allows, it is important to get this cancer cover plan as the coverage offered by just MyShield alone (5x MSL) will be insufficient.

Do drop me a WhatsApp if you would like to find out more.

Integrated shield plan will no longer offer ‘As-Charged’ coverage for cancer from 1st April. This is in line with the MOH policy and MediShield Life (MSL) changes.

For AIA Healthshield Gold Max A policyholders, do note the below coverage for drugs ON the cancer drug list:

AIA Cancer Coverage with the Cancer Care Booster: 21x MediShield Life Limit AIA Cancer Coverage without the Cancer Care Booster: 5x MediShield Life Limit

This AIA Cancer Care Booster Rider will be launched from 1st April. It is automatically added if you have the Vitalhealth/VitalCare Rider, on policy renewal.

If you do not have the rider, please note that we will have to apply for it separately. There is a window period for application without underwriting.

Conclusion: Beyond just covering for copayment, the rider is now a necessity if you want to be covered at a more relevant level. Even then, it may be prudent to consider an extra, standalone cancer rider. Do drop me a WhatsApp if you would like to find out more.

info updated as of 29th march – AIA increased the benefits of cancer booster

Integrated shield plan will no longer offer ‘As-Charged’ coverage for cancer from 1st April. This is in line with the MOH policy and MediShield Life (MSL) changes

For Income Enhanced Incomeshield Plan, do note that coverage will be based on the below for drugs on the cancer drug list.

If you have the main plan and rider (Deluxe Care Rider / Plus Rider / Classic Care Rider / Assist Rider)

(Private Hospital) Preferred Plan + Rider: 15x MSL Limit (Govt A Ward) Advantage Plan + Rider: 12x MSL limit (Govt B1 Ward) Basic Plan + Rider: 9x MSL Limit

If you have the Main IP plan only

(Private Hospital) Preferred Plan: 5x MSL Limit (Govt A Ward) Advantage Plan: 4x MSL limit (Govt B1 Ward) Basic Plan: 3x MSL Limit

Conclusion: Beyond just covering for copayment, the rider is now a necessity if you want to be covered at a more relevant level.

And while Incomeshield is still one of the most consistent and premium/coverage competitive plans available in the market. it may be prudent to consider a standalone cancer rider that can cover you more comprehensively. Whatsapp me at to find out more/

Once again, the tax season has arrived and if you have not filed your taxes yet, here are some key ways you can save on taxes, simply by maximising and allocating your tax reliefs.

Part 1: Upon tax reporting in March / April 2023:

(1) Course fee tax relief $5,500: Any course of study, seminar or conference in 2022 for the purpose of gaining an approved academic, professional or vocational qualification

(2) Life Insurance tax relief: $5,000: If your CPF contribution is < $5,000, you may claim the lower of: a. the difference between $5,000 and your CPF contribution; or b. up to 7% of the insured value of your own/your wife’s life, or the amount of insurance premiums paid New! The voluntary cash contribution to your Medisave account is not considered for the $5,000 limit for the total CPF contribution for YA 2023 onwards.

(3) Parents relief $9,000: You may claim this relief if you have supported the following dependants: a. Parents / Parents-in-law / Grandparents / Grandparents-in-law b. Stay with dependent $9000 / Don’t stay with dependent $5,500 TIP! You may also discuss with your siblings on how to share the parents relief.

(4) Qualifying Child Relief $4000: For parents, you may claim tax relief of $4,000 per child. TIP! Depending on your income, it may be better for QCR to be claimed under fathers, as mothers have Working Mother Child Relief

(5) Working Mother Child Relief: Percentage of income. For working mothers, you may claim up to 60% of your income depending on the number of children as below, and your child did not have an annual income exceeding $4,000. 1st Child: 15%, 2nd Child: 20%, 3rd Child: 25% of income. Tip! if your child worked part-time before tertiary education, your WMCR will be automatically removed. But you may write to IRAS to request to re-instate the WMCR once your child is back to full-time studies.

NEW! Budget 2023 – From YA 2025, there will be changes to WMCR from a percentage of income to a fixed amount. Budget 2023: Child relief for working mothers to be fixed from 2024

Click here for full list of reliefs. Do also note that there is an overall tax reliefs cap at $80,000

a tax is a fine for doing well a fine is a tax for doing wrong

Part 2: By end of the year 2023. Reliefs & deductions to reduce tax for 2024 NOA (to be done before 31/12/2023):

(1) Do good and save on taxes at the same time! Donations to approved Institution of a Public Character (IPC) enjoy tax deductions of 2.5 times the qualifying donation amount.

(2) CPF Cash Top Up Contribution Up $16,000: This is applicable if you top up to the CPF SA account if you have not reached the Full Retirement Sum. TIP! You can enjoy tax relief of up to $16,000 for cash top-ups made in each calendar year. Get up to $8,000 tax relief when you top up for yourself and up to $8,000 when you help your loved ones build their retirement savings.

For self-employed: Max contribution $37,740. You may contribute the maximum CPF contribution of $37,740 to reduce your taxable income Tip! You should top up as early as possible to benefit from the power of compound interest over the years.

(3) Supplementary Retirement Scheme $15,300: SRS is a tax deferment scheme. Every dollar contributed to your SRS account is eligible for SRS Tax relief the next year. Tip! You are able to invest the monies in your SRS, or put into saving vehicles like SSB, making it a great retirement accumulation tool.

Hop the above information is useful!

If you are still unsure about the tax reliefs or have any queries, drop me a WhatsApp

a financial review when the outlook of the economy is gloomy is more important than financial planning when things are rosy.

When times are bad (note that the list is not exhaustive):

Our income may be affected.

The risk of unemployment goes up.

Pay cuts happen.

Contract workers may not get renewed

Drop in revenue (affects business owners)

Expenses may go up

Think rent, mortgages, petrol and even food prices. There are many news regarding this recently so I shall not elaborate.

Tougher borrowing terms

You may not be able to get financing easily

In the event of a drop in asset prices/loss of income, you may not even be able to refinance your loans

A financial review will help you assess your capacity to deal with any of the above scenarios, and allow you to make adjustments to improve your situation.

And step 1: awareness on your spending habits. What are you REALLY spending on?

First, calculate your monthly fixed expenses. This includes bills and payments which HAVE to be paid and which remain fairly consistent in the short term – this means you can’t just make huge cuts just because you want to.

Think rent & mortgage repayments- even if you were to make lifestyle choices and move to a more modest home, the process takes time. This is also the reason why the government has the mortgage servicing ratio and total debt servicing ratio in place to ensure financial prudence.

If a huge chunk of your income is going to fixed expenses, you may find yourself in a more stressful situation in the event of a pay cut/unemployment as it would require you to make major lifestyle changes to bring down the expense to fit the budget (or a smaller income)

To mitigate this, keep enough emergency cash or have a plan that can buy you time (such as renting out a room in the house, moving in with your parents temporary, exercising retrenchment benefits/premium holiday on your insurance plans).

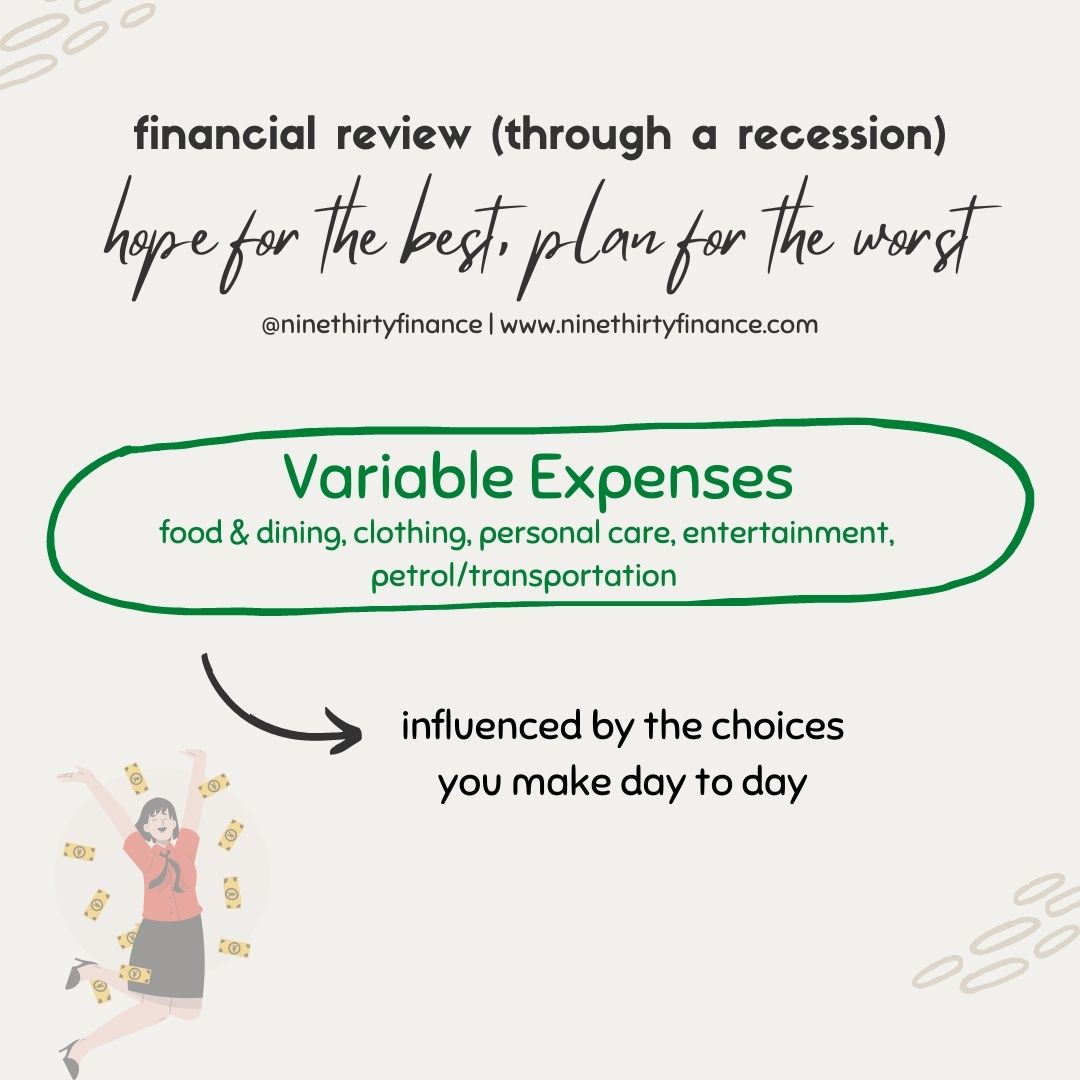

Next up, calculate your monthly variable expenses. This includes discretionary spending that can be reduced easily.

Food – Dining in vs preparing your own meals For some people, dining out could be cheaper as it may not be cost effective to cook for one. For others, having their meals at home can save a huge chunk.

Transport – Public transport vs driving/taking the taxi

and the list goes on.

The good news if a large part of your income goes to discretionary spending is that you can easily make adjustments when times are bad. The bad news is that human beings are creatures of habit and it can be painful to change your spending habits overnight.

If you are working in a high risk sector, you may want to start assessing your spending habits in order to be better prepared.

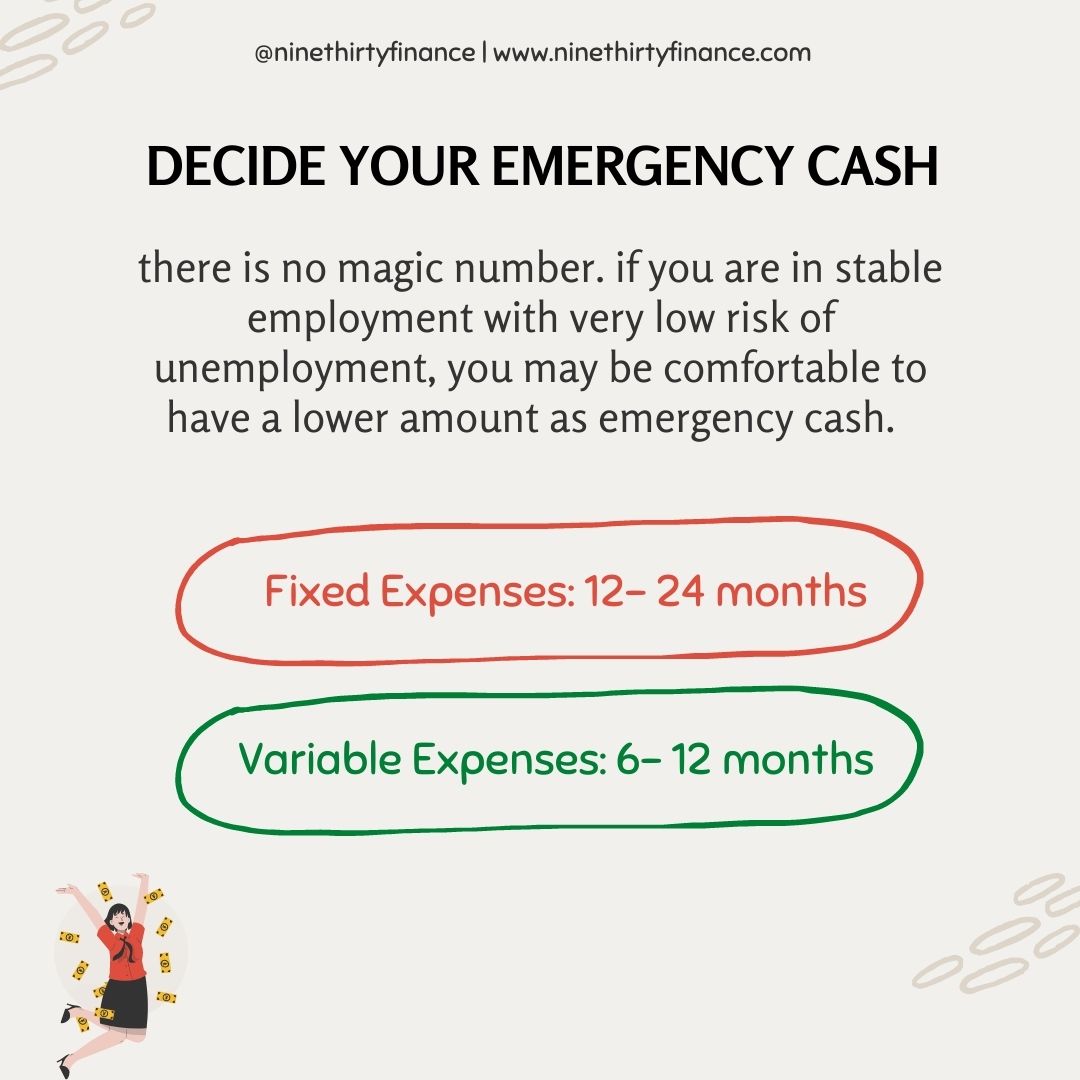

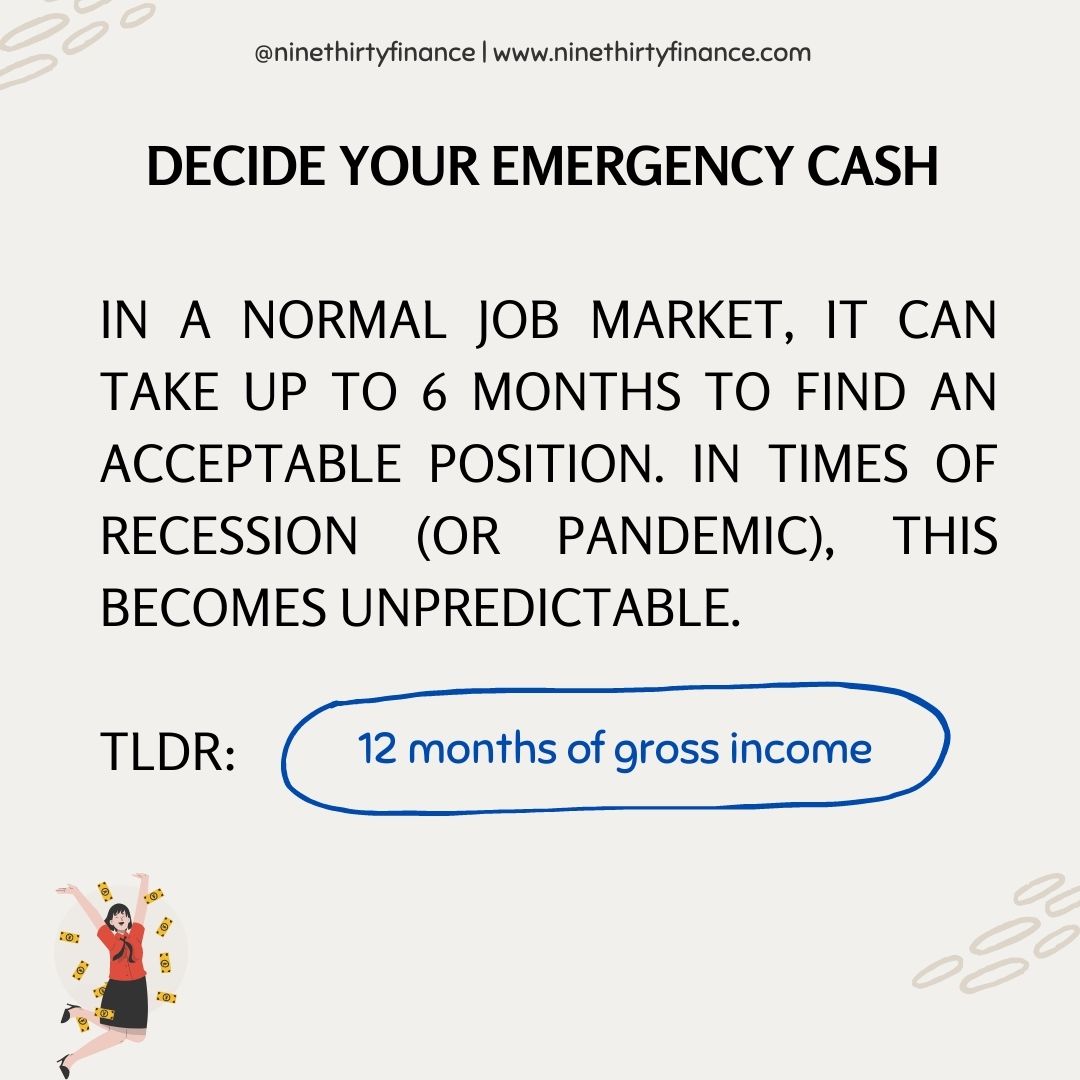

The whole point of calculating your expenses? To help you determine the level of emergency cash to keep. (No, I do not think that the commonly advocated emergency cash of 3-6 months expense is sufficient)

Of course, if you still aren’t convinced to do this ‘tracking exercise’, just keep 12 months of your income as emergency cash.

The Singapore Savings Bonds is currently giving a high interest rate of ~3.4%p.a. As it is a highly liquid vehicle, it is a great vehicle to use to hold your emergency cash. And the reason why I advocate this over FD/T-bills is because i do not believe that interest will stay at a high level (not 10 years, anyway) perpetually.