Many government insurance/medical schemes have been adjusted in recent years. The latest change involves cancer treatment coverage under our Medishield Life + Integrated shield plans.

Summary

The Ministry of Health (MOH) announced that there will be changes to cancer drug treatments and this move will support the procurement of cancer drugs at better prices and help to keep MediShield Life premiums sustainable.

- More cancer patients will be subsidised for their outpatient drug treatment

- 90% of the existing cancer drug treatments used in the public sector will be included in the positive list of cancer drug treatments that are claimable under MediShield Life (Yay!)

- Certain treatments will either no longer be claimable or have the claim limit lowered with no subsidy extended (nay 😦 )

- Changes will take place from September 2022.

Currently, private integrated shield plans provide as-charged coverage for outpatient cancer drug treatments, subjected to an overall policy year limit.

To encourage the use of clinically proven and cost-effective cancer drug treatments, Integrated Shield plans will be required to only cover treatments that are on the MediShield Life positive list and set claim limits for each cancer drug treatment. According to MOH, the move will apply to all Integrated Shield Plans sold or renewed from April 2023 onwards. Claims cannot be made for drugs not on the list.

I would say that this change is for the better for most people as the overall cost of most cancer treatment will go down. However, for individuals who would prefer greater control over their treatment plans, this may come as a blow (as ~10% of the drugs may be covered only up to claim limits/ not at all).

How should you manage your financial portfolio with this change?

- If you already have a whole life plan that pays a lump sum on Critical Illness, it will be ideal to hold the plan for life rather than cashing it out for the surrender value

- Review and make sure that your current Critical Illness coverage is sufficient OR set aside more emergency cash to provide for situation where you wish to receive treatment/drugs not on the positive list.

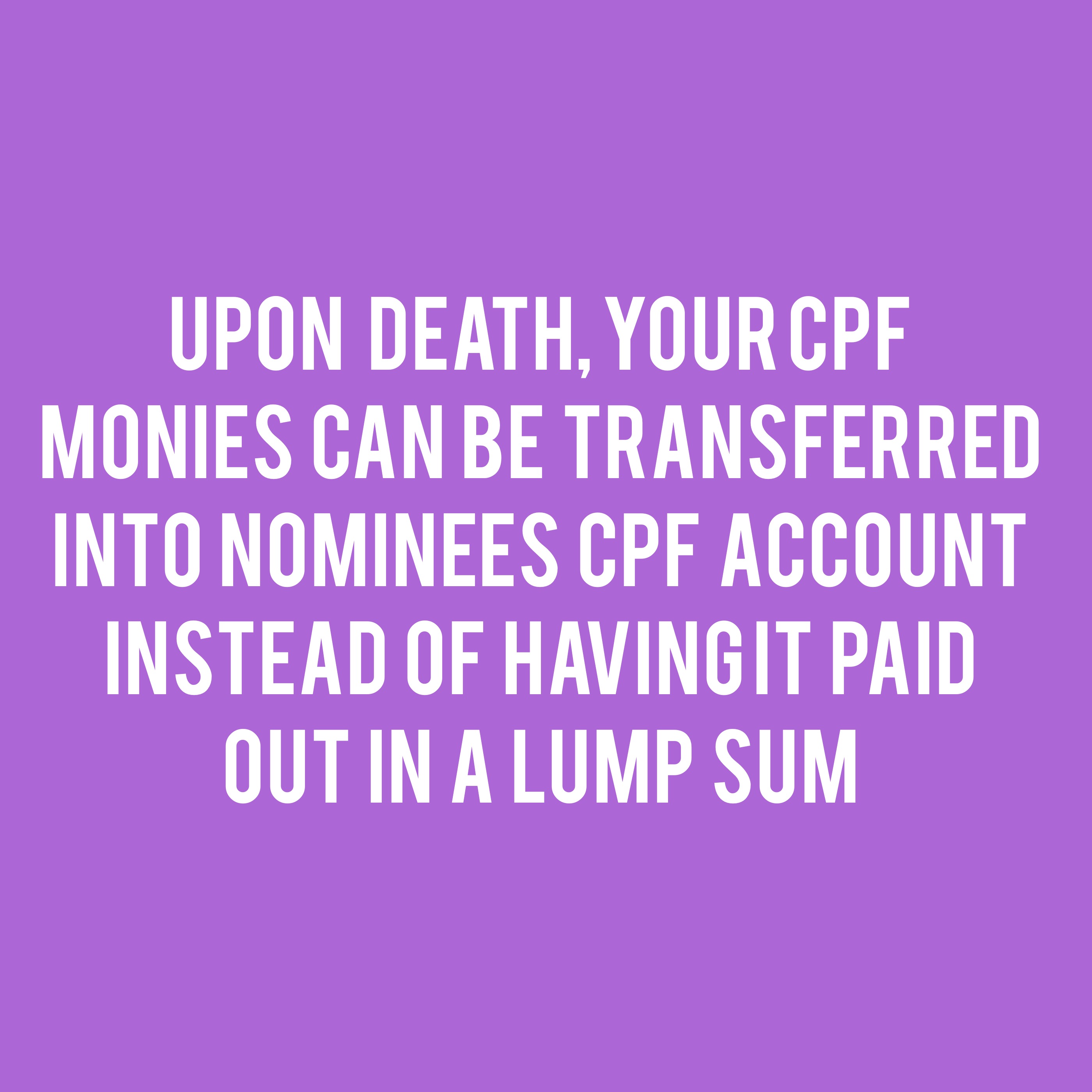

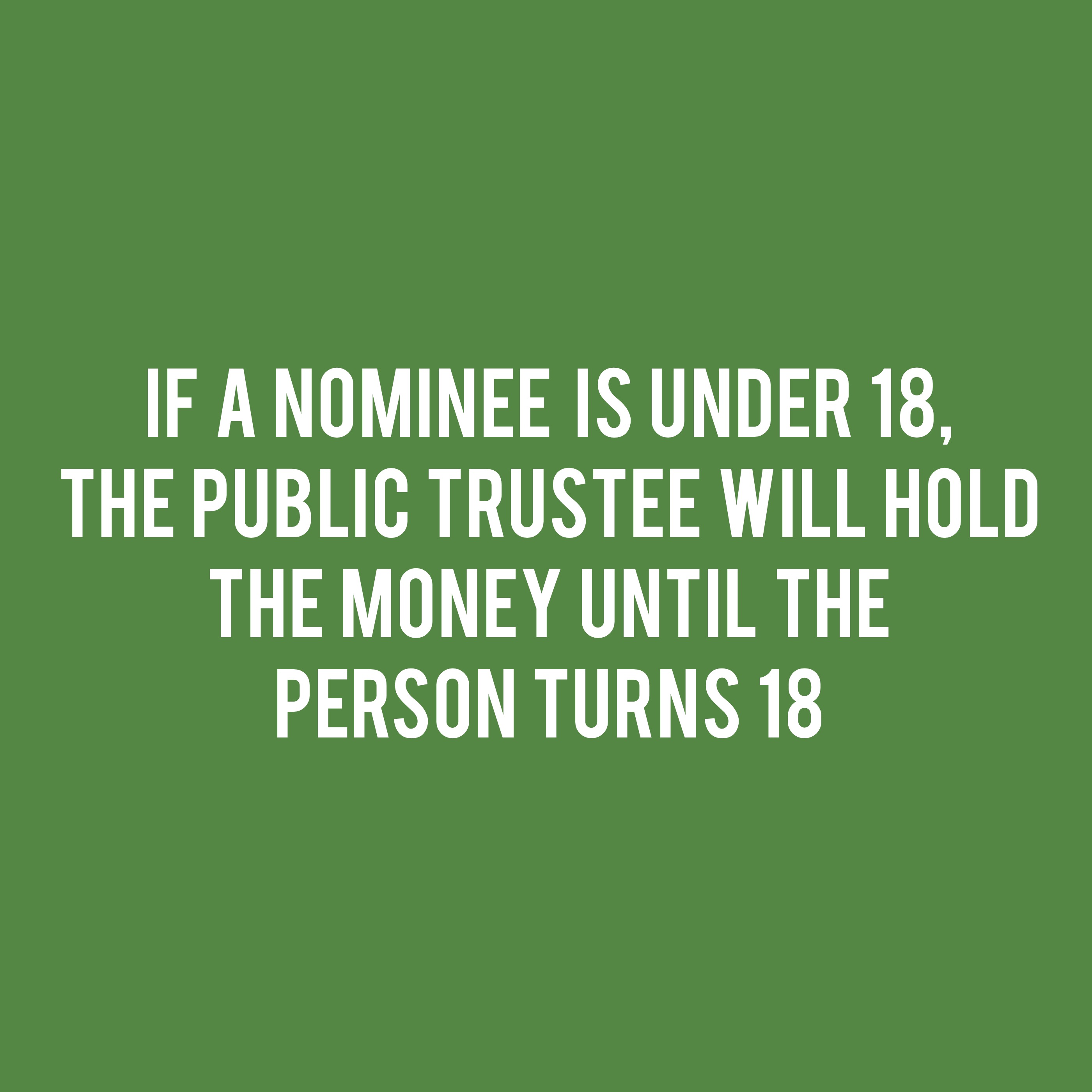

Unknown to many, CPF actually has the special needs saving scheme that can help parents of children with special needs to save for their long-term care needs. Parents can nominate their children to receive monthly disbursements from the parent’s CPF savings after death. This scheme is administered by the Special Needs Trust Co and is probably worth looking at if of relevance.

Unknown to many, CPF actually has the special needs saving scheme that can help parents of children with special needs to save for their long-term care needs. Parents can nominate their children to receive monthly disbursements from the parent’s CPF savings after death. This scheme is administered by the Special Needs Trust Co and is probably worth looking at if of relevance.