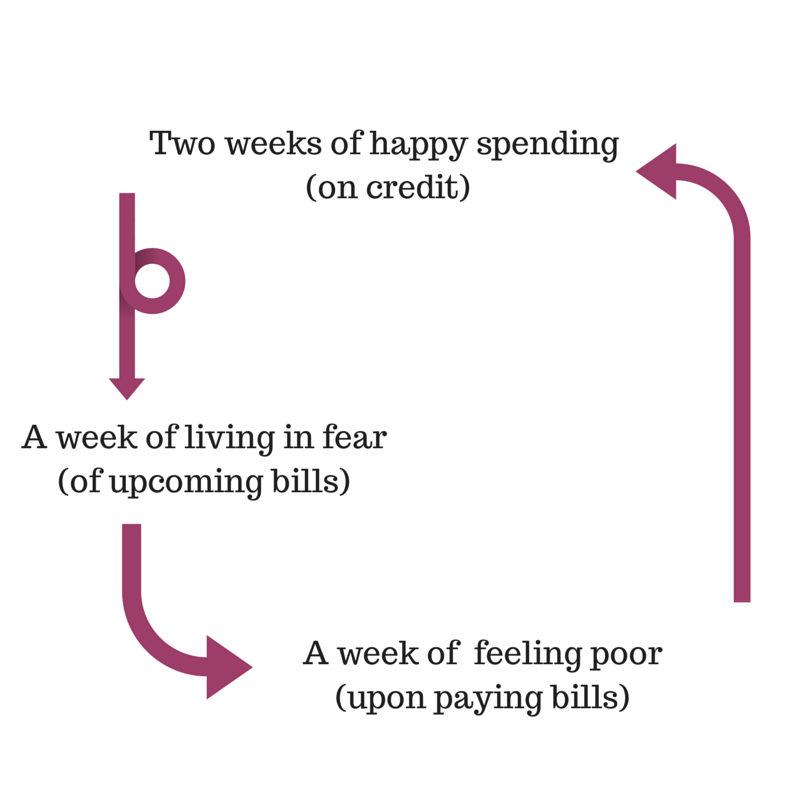

Recently, I spoke to a client (a teenager) on her spending habits. This is her description on how she feels on a monthly basis:

Countless research and poll have shown that it is much easier to overspend with this mode of payment because when we sign off the plastic, we do not experience (visually) that we are spending- our bank account value does not decrease, the cash in our wallet remains as it is. Sometimes, we are even lured into a false sense of security of having more money, for example in the case where friends return you their share of the expenses charged to your card – but which becomes money which you eventually spend (on yourself). Sometimes, we convince ourselves that we are enjoying the rebates/discounts of the credit card company – which is all true until when the bill date draws nearer and we realise that we have spent more than what we should have.

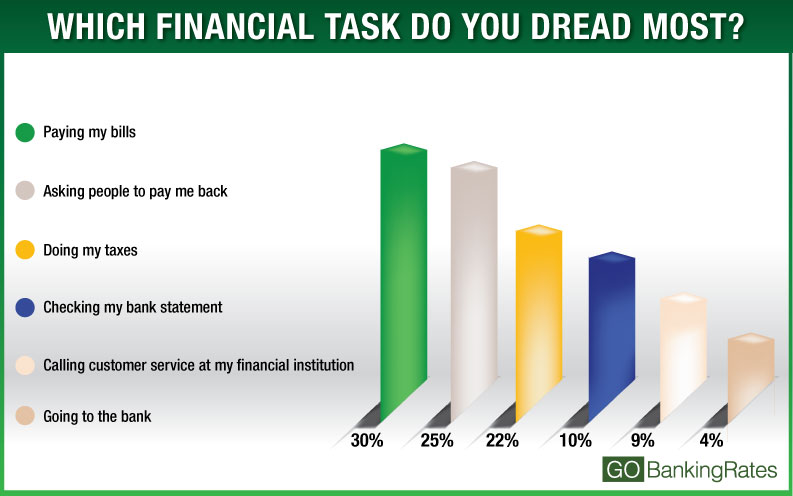

Then, the dread comes. The fear of paying the bills is not uncommon. A poll conducted by gobankingrates.com (US site on interest rates of financial services) shows that of the various financial tasks, people dread paying the bills the most.

This vicious cycle is more than just an emotional roller-coaster. The cycle itself does not promote good habits because we spend before we save. What we really need, is to cultivate a healthier habit. And here are 3 steps that will lead you to that.

#1. Pay yourself first (Accumulation Account)

Internet banking has made it really easy to schedule bank transfers so what I advocate, is to pay yourself FIRST. This means setting up a separate account, and putting money away into that account on the day you receive your pay. The amount that I set aside into this account is based on my:

– Monthly investment amount (For long term goal; regular investment for Dollar Cost Averaging advantage)

– Monthly insurance premium (For long term goal; insurance savings plan for stability)

– Monthly insurance premium (Life insurance for wealth protection)

– Monthly general savings

– Monthly targeted savings (wedding/house/business)

I also set up my giro arrangements such that insurance premium/investments are deducted from this account. This way, you know exactly how much you are saving and you know you will never miss the important payments. You also ensure that your long term goals will never be jeopardise by a moment of temptation. In my opinion, the amount should be at least 40% of your take-home income.

(So basically, this is my accumulation account and my income debiting account is my expenses account)

#2 Pay off your fixed bills next (Expenses Account)

Some of our bills are fixed, while some are variable. Personally, I schedule all my fixed expenses to be paid to the respective billing organisation 1 day after my pay day. These includes mobile phone, internet, utilities, household, motor/mortgage repayments, fixed credit card instalments (if you have purchased any big ticket items on your card) and dependents’ expenses.

It is important to do this first, because once this is done, you know that you can spend freely for whatever that is left in your income debiting account.

#3 Pay off credit card expenses immediately (Expenses Account)

And I mean immediately. If you would like to use your credit cards because of the rebates/discounts, then pay it off once the expense has been charged. Log on to your ibanking mobile app and make that payment NOW- if you can surf instagram and facebook, you can do this too.

By doing so, you get your discounts and rebates and you do so without the dread of paying a huge bill at the end of the month. More importantly, you cut the risk of overspending.

This process may seem harsh but it is liberating because you never have to worry about the bills and it will always keep you out of debt. (Look out for our upcoming post to learn how to get yourself out of debt first)

Lastly, I personally let the money in this Expenses Account roll. Then, I splurge on myself whenever the amount builds up. For me, it will always be on an air ticket but it could be anything for you- just as long it is a source of motivation for you to spend wisely 😉